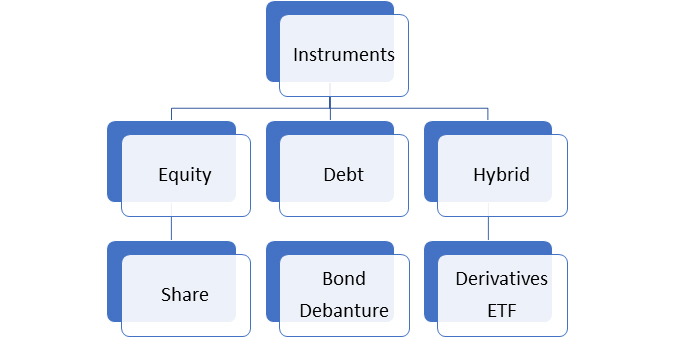

EQUITY SHARES:

- An equity share signifies ownership in a company, granting the shareholder partial ownership rights.

- Shareholders typically acquire voting rights in significant corporate matters and may receive dividends, a portion of the company’s profits.

- Additionally, the value of equity shares appreciates if the company experiences growth, presenting the opportunity for capital gains.

Preferential shares

- It is known as preference shares, which are issued by a company that gives the shareholders certain preferential rights over common shareholders.

- These rights often include a fixed dividend that must be paid before dividends can be distributed to common shareholders.

- Additionally, preferential shareholders may receive first priority in the event of liquidation of the company.

- However, they typically do not have voting rights or the same level of influence as common shareholders in corporate decision-making processes.

Promoters’ shares

- It refers to the portion of company shares held by a company’s founders or initial organizers.

- These shares are often acquired at the company’s inception or during its early stages of development. Promoters typically hold a significant stake in the company and play a crucial role in its establishment and growth.

- They are usually involved in the management and decision-making processes of the company. Promoters’ shares may also come with certain privileges or rights, such as voting rights and the ability to influence strategic decisions.

Sweat Equity

- Sweat equity refers to the contribution made by employees or founders to a company through effort, labour, or services, rather than through monetary investment. In return for their contributions, individuals are typically rewarded with equity or shares in the company.

- This equity represents a form of compensation for the value added by the individual’s work or expertise.

- Sweat equity is often used in startups or early-stage companies where cash resources may be limited, allowing employees or founders to share in the potential success and growth of the company based on their contributions.

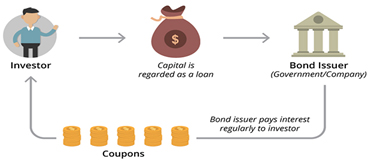

BOND

- A bond is a debt instrument where an investor lends money to an entity, typically a corporation or government, for a defined period at a fixed or variable interest rate.

- Bonds are utilized by various entities, including companies, municipalities, states, and sovereign governments, to raise funds for different projects and activities. Bondholders become creditors of the issuer.

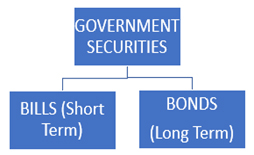

Government Securities (G-Sec)

- A Government Security (G-Sec) is a tradable instrument issued by the Central or State Governments, acknowledging the government’s debt obligation.

- RBI issues it on behalf of the government of India. It is issued to borrow funds from the market for short-term or long-term requirements.

- G-Secs are considered risk-free gilt-edged instruments due to their minimal risk of default. It is called Gilt-edged because it is issued in golden coloured edge.

- Types of government security:

- Short-term: such as treasury bills with original maturities of less than one year.

- Long-term: such as government bonds or dated securities with maturities of one year or more.

- In India, the Central Government issues both treasury bills and bonds, while State Governments issue bonds, known as State Development Loans (SDLs).

Types of Government Bond

Fixed-Rate Bonds:

- These are bonds on which the coupon rate (interest rate) is fixed for the bond’s entire life (i.e., till maturity). Most Government bonds in India are issued as fixed-rate bonds.

- For example, the 8.24% government bond 2025 was issued in 2015 for a tenor of 10 years, maturing in 2025. Coupons on this security will be paid half-yearly at 4.12% (half-yearly payment being half of the annual coupon of 8.24%) of the face valuer.

Floating Rate Bonds (FRB)

- FRBs are securities which do not have a fixed coupon rate. Instead, it has a variable coupon rate, which is re-set at pre-announced intervals (say, every six months or one year).

- FRBs were first issued in 1995 in India.

Zero Coupon Bonds:

- Zero coupon bonds are bonds with no coupon (interest) payments. However, like T-bills, they are issued at a discount and redeemed at face value.

- The Government of India had issued such securities in 1996. It has not issued zero-coupon bonds since then.

Capital Indexed Bonds

- These are bonds, the principal of which is linked to an accepted inflation index to protect the investors’ Principal amount from inflation.

- A 5-year Capital Indexed Bond was first issued in December 1997 and matured in 2002. Later on, the same bond was issued under the name Inflation-indexed bond.

Inflation Indexed Bonds (IIBs)

- IIBs are bonds wherein both the interest and the principal amounts are protected against inflation.

- Globally, IIBs were first issued in 1981 in the UK. In India, the government issued IIBs through RBI in 2013. Since then, they were issued monthly (on the last Tuesday of each month) till the end of 2013.

- Based on the success of these IIBs, the Government of India, in consultation with RBI, issued the IIBs (CPI-based) exclusively for retail customers.

- Coupons are paid midyear. The calculated coupon rate shall be reimbursed on an adjusted principal.

- The minimum individual investment is Rs 5000, with a maximum of Rs 10 lakh per year. The maximum institutional investment is Rs 25 lakh per year.

- To illustrate the workings of Inflation-Indexed Bonds, consider an example:

- Assume an investor acquires an IIB with a face value of Rs. 10,000, a ten-year maturity, and a coupon rate set at 3% above inflation. In the first year, if the inflation rate is 4% at the bond’s issuance, the investor receives an annual interest payment of Rs. 312 (3% of INR 10,400).

- If the inflation rate rises to 5% in the second year, the investor would receive an annual interest payment of Rs. 327.60 (3% of INR 10,920 ( 5% of 10 400=10920)). Importantly, the coupon rate remains consistently set at 3% above the inflation rate throughout the ten-year duration.

State Development Loans (SDLs)

- State Governments also raise loans from the market called SDLs. SDLs are dated securities issued through normal auctions similar to those conducted for dated securities issued by the Central Government

- Interest is serviced at half-year intervals, and the principal is repaid on maturity.

- Like dated securities issued by the Central Government, SDLs issued by the State Governments also qualify for SLR.

- State Governments have also issued special securities under the “Ujjwal Discom Assurance Yojna (UDAY) Scheme for Operational and Financial Turnaround of Power Distribution Companies (DISCOMs).”

Sovereign Gold Bond (SGB) Scheme

- SGBs are government securities denominated in grams of gold. The RBI issues the bond on behalf of the GOI. The SGB Scheme was first launched by the GOI in 2015.

- They are substitutes for holding physical gold. Investors have to pay the issue price, and the bonds will be redeemed upon maturity.

- Who is eligible to invest in the SGBs?

- The bonds will be restricted for sale to resident Indian entities, including individuals (in their capacity as individuals, or on behalf of a minor child, or jointly with any other individual), Hindu Undivided Family (HUF), Trusts, Universities, and Charitable Institutions.

- What are the minimum and maximum limits for investment?

- The bonds are issued in denominations of one gram of gold and multiples thereof.

- The minimum investment in the bond shall be one gram, with a maximum subscription limit of 4 kg for individuals, 4 kg for HUFs, and 20 kg for trusts and similar entities notified by the government from time to time per fiscal year.

- Tenor:

- The bond’s tenor will be for eight years, with an exit option in the 5th, 6th, and 7th years, to be exercised on the interest payment dates.

- Interest rate

- The investors will be compensated at a fixed rate of 2.50% per annum, payable semi-annually on the nominal value (face value or stated value)

- Other Features:

- Payment for the Bonds will be through cash payment, demand draft, cheque, or electronic banking.

- Investors are assured of the market value of gold at the time of maturity and periodical interest.

- These securities can be used as collateral for loans from banks and Non-Banking Financial Companies (NBFCs).

- Bonds will be tradable on stock exchanges.

- Bond interest will be taxable per the Income-tax Act, 1961 provisions. However, the capital gains tax arising on the redemption of SGB to an individual has been exempted.

Other types of bonds

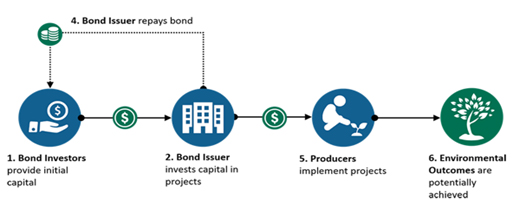

Green bonds

- It is an instrument used to raise capital specifically for funding environmentally friendly projects related to renewable energy, clean transportation, and sustainable water management.

- The World Bank issued its first green bond in 2008. Over time, in 2013, corporations also began participating in issuing green bonds, leading to their overall expansion and popularity.

- The Indian government also issued sovereign green bonds as a part of its borrowing program. The government issued the framework for the sovereign green bond in 2022.

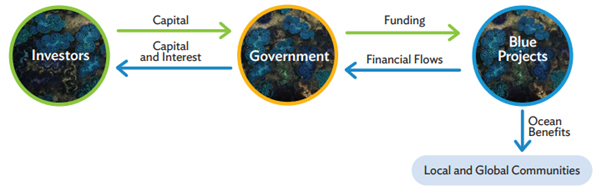

Blue Bond:

- Blue bonds are innovative financial tools aimed at supporting sustainable marine and fisheries initiatives. They fall under the category of green bonds, with the World Bank defining them as debt instruments issued by governments, development banks, or other entities to secure funding from impact investors for marine and ocean-related projects that offer environmental, economic, and climate-related advantages.

- The Republic of Seychelles made history in 2018 by introducing the world’s inaugural sovereign blue bond.

Masala Bond

- Masala Bonds are debt instruments denominated in Indian rupees and issued outside India. They serve as a means for raising funds in the local currency from foreign investors.

- Payment for both the coupon and principal of Masala Bonds is made in Indian rupees, not in the currency of the foreign investors. Therefore, the investor bears the currency risk associated with fluctuations in exchange rate.

- Indian companies find raising funds through Masala Bonds advantageous because they typically secure lower interest rates than borrowing within India. This is because interest rates in developed markets, where these bonds are often issued, tend to be lower.

- The first Masala bond was issued in 2014 by the International Finance Corporation (IFC) for infrastructure projects in India.

- Similar bonds are Panda Bonds, Kangaroo Bonds, Bulldog Bonds, Samurai Bonds, Yankee Bonds, etc

- Investors:

- These bonds are exclusively available to residents of countries that are members of the Financial Action Task Force (FATF).

- Additionally, the country’s security market regulator must be a member of the International Organization of Securities Commissions (IOSCO).

- Maturity Period:

- Bonds with a fundraising amount of up to 50 million US Dollars equivalent in INR per financial year must have a minimum original maturity period of 3 years.

- Bonds with a fundraising amount exceeding 50 million US Dollars equivalent in INR per financial year must have a minimum original maturity period of 5 years.

- Eligibility:

- It can be issued by investors ranging from government, banks, corporations, etc. Investors from outside India who express interest in investing in Indian assets are also eligible to invest in Masala bonds.

Additional Tier 1 (AT1) Bond

- AT1 bonds are a type of perpetual bond issued by banks to strengthen their capital base. Banks issue AT1 bonds to raise capital and enhance their Tier 1 capital ratios, which are regulatory measures of a bank’s financial strength and ability to absorb losses.

- Perpetual Nature:

- Unlike traditional bonds with a fixed maturity date, AT1 bonds have no maturity date. They are perpetual, meaning they have no specific redemption date and can remain outstanding indefinitely.

- Coupon Payments:

- AT1 bonds typically pay a fixed or floating rate of interest, known as the coupon, which is paid periodically to investors. However, banks have the discretion to defer coupon payments if they face financial stress or if regulatory requirements are not met.

DEBENTURE

- Debenture is a debt instrument not secured by physical assets or collateral. Instead, it is backed only by the general creditworthiness and reputation of the issuer.

- Debentures typically offer a fixed interest rate and have a specified maturity date at which the principal amount is repaid to the debenture holders.

- Types:

- Convertible Debentures:

- Provide the holder the option to convert them into equity shares or other securities at a predetermined ratio and price.

- They can be either fully convertible, meaning they can be converted into equity shares entirely, or partially convertible, where only a portion of the debenture can be converted.

- Non-Convertible Debentures:

- Non-convertible debentures are debt instruments that cannot be converted into equity shares or other securities.

- These debentures offer a fixed interest rate to the debenture holders throughout the tenor of the debenture.

- Non-convertible debentures are the most common type of debentures issued by companies.

- Convertible Debentures:

HYBRID INSTRUMENT

- Hybrid instruments refer to financial securities that hold the features of equity and debt These instruments possess stocks (equity) or bonds (debt) characteristics, offering investors a unique blend of risk and return profiles.

Mutual Fund

- A mutual fund is a pooled investment that collects money from multiple investors and invests it in a diversified portfolio of securities such as stocks, bonds, money market instruments, or a combination of these assets.

- The fund is managed by professional portfolio managers who make investment decisions on behalf of the investors

- Advantages:

- Professional Management: The fund managers research for you. They select the securities and monitor their performance.

- Diversification: meaning “Don’t put all your eggs in one basket.” Mutual funds typically invest in a range of companies and industries. This helps to lower your risk if one company fails.

- Affordability: Most mutual funds set a relatively low amount for initial investment and subsequent purchases.

- Liquidity: Mutual fund investors can redeem their shares anytime for the current net asset value (NAV) plus redemption fees.

- Classification:

- Open-ended: These mutual funds allow you to invest and redeem investments anytime. They are perpetual in nature, liquid in nature, and don’t have a specific investment period.

- Close-ended: These schemes have a fixed maturity date. You can only invest at the time of the new fund offer, and redemption can only be made on maturity. You cannot purchase the units of a close-ended mutual fund whenever you please.

Exchange-traded fund (ETF)

- ETFs are funds that bundle together different assets like stocks, bonds, or commodities. They’re like a basket of investments.

- ETFs are made for investors who want diversity in their portfolios without buying each asset separately.

- Unlike mutual funds, ETFs can be traded on stock exchanges throughout the day, just like individual stocks.

- Advantages of ETFs:

- Flexibility: ETFs can be bought and sold throughout the day, allowing investors to react to market movements and news in real-time.

- Transparency: Most ETFs are required to disclose their holdings daily, allowing investors to see exactly what assets they own, enhancing transparency and informed decision-making.

- Tax Efficiency: ETFs tend to be more tax-efficient than actively managed mutual funds because they typically generate fewer capital gains distributions, resulting in potential tax savings for investors.

- Trading Options: Since ETFs are traded on stock exchanges, investors can use various order types, such as limit orders or stop-loss orders, providing more control over their investment strategies than traditional mutual funds.

Central Public Sector Enterprises (CPSE) Exchange Traded Fund (ETF)

- The government launched the Central Public Sector Enterprises (CPSE) Exchange Traded Fund (ETF) in 2014.

- The CPSE ETF operates similarly to a mutual fund scheme and includes shares from 10 public sector undertakings (PSUs), namely ONGC, Coal India, IOC, GAIL (India), Oil India, PFC, Bharat Electronics, REC, Engineers India, and Container Corporation of India.

- Minimum investment amount for CPSE ETF is ₹5000. There is no lock-in period for your investment, and being an open-ended scheme, one can easily trade the fund units on the stock exchanges of India.

Bharat – 22

- Bharat 22 is an Exchange-Traded Fund (ETF) designed to mirror the performance of 22 stocks from various sectors. These stocks include Central Public Sector Enterprises (CPSEs), Public Sector Banks (PSBs), and strategic holdings of SUUTI (Specified Undertaking of Unit Trust of India).

- The 22 stocks are spread across six sectors: basic materials, energy, finance, FMCG (Fast Moving Consumer Goods), industrials, and utilities, providing investors with diversified exposure to the Indian market.

Bharat Bond ETF

- The Bharat Bond ETF is a collection of bonds issued by various government entities such as CPSEs, CPSUs, and CPFIs. It offers units at a minimal size of ₹1,000, enabling even retail investors to participate.

- Each ETF has a set maturity date, and initially, there are two series available: one with a 3-year maturity and the other with a 10-year maturity. Each series corresponds to a distinct index based on its respective maturity period

Derivative

- A derivative is a financial contract or instrument whose value is based on the price of an underlying asset, such as stocks, bonds, commodities, or currencies. It derives its value from changes in the price of the underlying asset.

- They let people bet on or protect against changes in the value of these things without actually owning

- Common types:

- Futures Contracts: Futures contracts require the buyer to purchase and the seller to sell a specific amount of an asset at a set price on a future date. They are standardized and traded on organized exchanges.

- Options: Options give the holder the right, but not the obligation, to buy (call option) or sell (put option) an asset at a set price within a specific period. The buyer pays a premium for this right.

- Swaps: Swaps are agreements between two parties to exchange cash flows or other financial instruments based on set terms. Common types include interest rate swaps, currency swaps, and commodity swaps.

- Forwards: Forwards are custom contracts between two parties to buy or sell an asset at a set price on a future date. Unlike futures, forwards are traded over-the-counter (OTC) and are not standardized.